Let’s unpack how Social Security benefits are calculated. The more I speak on Social Security, the more I realize that nobody really understands how the Social Security Administration (SSA) comes up with the numbers for the benefits provided.

I put this piece together to unpack precisely how the SSA calculates the full retirement age (FRA) benefit amount referred to as primary insurance amount (PIA).

I fear this might be a little “in the weeds.” But there’s no other way to explain it, so let’s dive in.

Three Amounts Used for Social Security Calculations

When a person gets their Social Security statement, it usually has three different amounts listed. Some additional amounts listed include Social Security disability, survivor’s benefit, and more, but the first three are used for calculations.

- The first amount is the age 62 benefit. This age is the earliest one can elect to take benefits. However, it reduces by 25-30% with this option.

- The second amount is the PIA. This number is determined by birth year and indicates when someone is eligible for the full-benefit amount.

- The third amount listed is the age 70 benefit. This amount includes the 5.5-8.0% delayed retirement credits a person receives if they wait to take benefits.

Related: 23 Crucial Years & 10 Birthdays That Impact Retirement Income

How Social Security Creates Eligibility Amounts

The age 62 and age 70 benefits are calculations from the PIA.

If someone takes their benefits before their FRA, they’ll be reduced by a certain percentage depending on their age (including month) when they begin taking it. If they delay their benefits, the opposite occurs, and they’ll receive an additional percentage for each year until age 70.

As you can see, the PIA is quite an important number. That poses the more important question: How is the PIA decided?

First, recognize that workers pay into Social Security every year they work. Their wages dictate how much goes into Social Security. There’s a maximum amount per year allowed to pay into Social Security. Starting in 2023, the maximum earnings subject to the Social Security tax is $160,200.

The PIA calculation takes a person’s highest 35 years of wages paid into Social Security and adjusts it for inflation. Each year has a different inflation factor. It’s also worth noting that any wages made starting at age 60 can be used as part of the highest 35 years, but that’s not adjusted for inflation.

Next in the calculation is to take the inflation-adjusted numbers and add them together. Divide the sum by 420—representing the total number of months in 35 years. This results in one monthly number called the average indexed monthly earnings (AIME).

Stick with me, this is where it can get muddy.

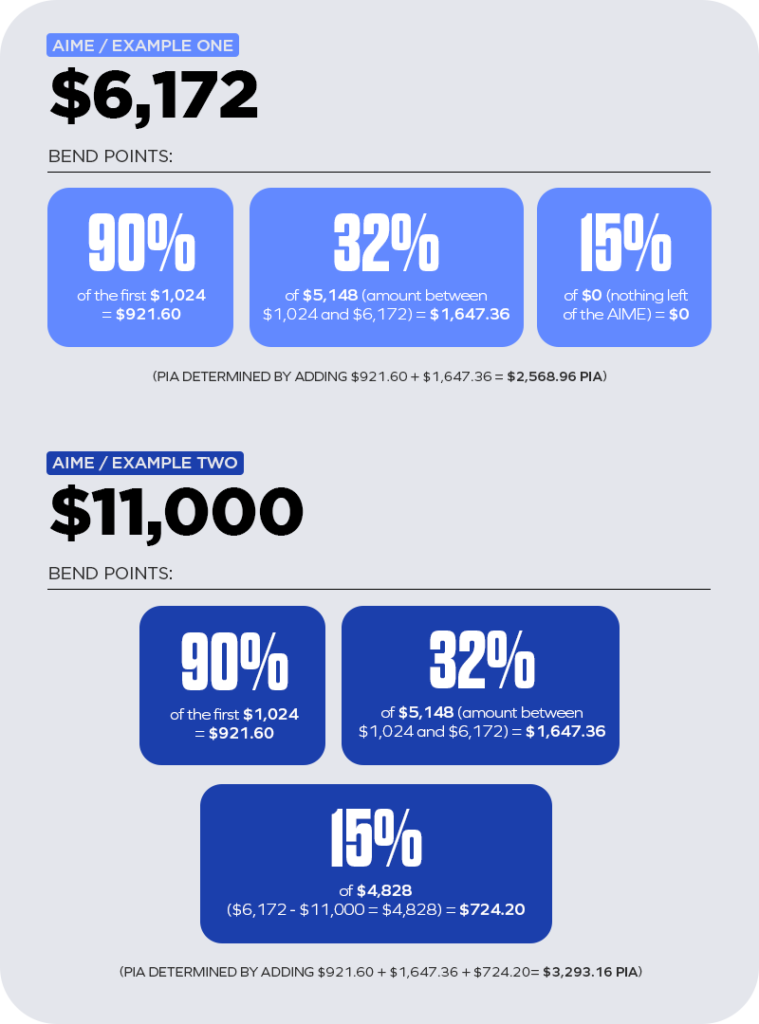

Next, the AIME runs through bend points, essentially income intervals that earn specific returns. There are three bend points, and they can change every year. Additionally, the bend points don’t lock in for an individual until the year that person reaches age 62.

Current Social Security Bend Points in 2023

- First bend point: 90% of the first $1,024 of the AIME

- Second bend point: 32% of the amount between $1,024 and $6,172 of the AIME

- Third bend point: 15% of whatever’s left of the AIME

Related: 10 Pieces of Retirement Planning Advice Retirees Wish They Had Known Sooner

Social Security Bend Point Examples

Reminder: These bend points could change yearly and won’t lock in for an individual until they reach age 62. As a result, statement amounts can fluctuate a lot during working years or until after age 60. So, retirement income planning requires a keen eye for strategy and a bit of flexibility.

Final Thoughts on Social Security Benefit Calculations

One final caveat surrounds workers who paid into Social Security for a period and then took a job (state or federal) where they didn’t pay into the program. These people fall under the Windfall Elimination Provision and, as it relates to spousal or widow benefits, Government Pension Offset. This is another discussion for another time.

Social Security and its benefits calculations are difficult if you’re not up to speed with all the rules and changes. It can make sense to reach out to a Social Security strategist, like we offer to our partnered financial professionals at Financial Independence Group.

Getting expert help can save you time and headaches, plus you won’t have to wade through all the minor details—empowering you to make the best retirement planning decisions for your clients.